Complete Guide to Trucking General Liability Coverage

Trucking general liability insurance is the cornerstone of commercial fleet protection, providing essential coverage for public liability, property damage, and regulatory compliance that every trucking operation needs to succeed.

Understanding Trucking General Liability Insurance

Trucking general liability insurance protects commercial trucking companies and owner-operators from financial losses arising from third-party claims of bodily injury, property damage, and other liabilities that occur during business operations. Unlike personal auto insurance, trucking general liability coverage is specifically designed to address the unique risks and regulatory requirements faced by commercial transportation companies.

This specialized coverage goes beyond basic vehicle insurance to protect against a wide range of business-related liabilities, including accidents during loading and unloading operations, damage to customer property, and claims arising from advertising activities. For trucking companies operating under Department of Transportation (DOT) authority, general liability insurance is not just recommended—it's often legally required.

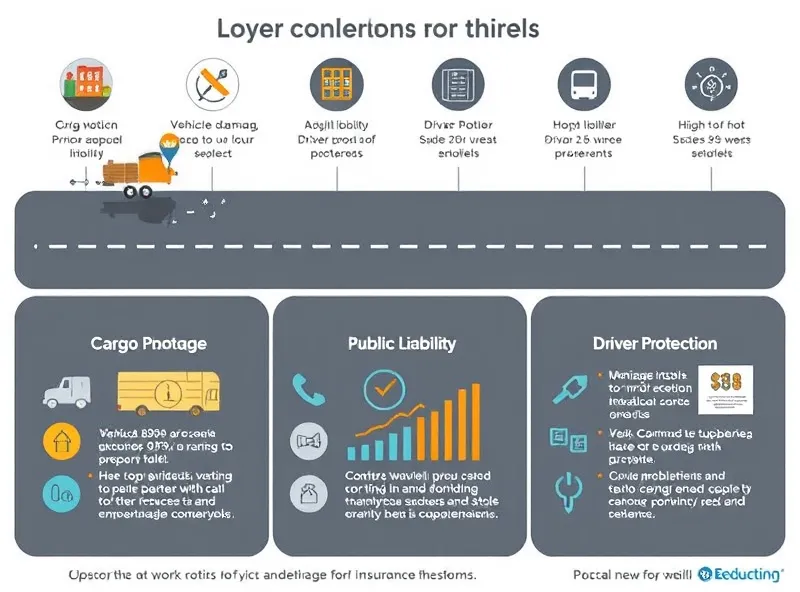

Key Components of Trucking General Liability Coverage

Bodily Injury Liability: This fundamental component covers medical expenses, lost wages, and pain and suffering when your trucking operations cause injury to third parties. Coverage typically ranges from $1 million to $5 million or more, depending on the nature of your cargo and operations.

Property Damage Liability: Protects against damage to other people's property, including vehicles, buildings, cargo, and infrastructure. This is particularly important for trucking companies that operate in urban areas or handle valuable freight.

Personal and Advertising Injury: Covers claims related to libel, slander, false advertising, and violations of privacy rights. While less common in trucking, this coverage is essential for companies that engage in marketing activities or have customer-facing operations.

Medical Payments: Provides immediate coverage for medical expenses of injured parties, regardless of fault. This coverage helps maintain goodwill and can prevent small incidents from escalating into larger liability claims.

DOT Requirements and Federal Compliance

Commercial trucking companies operating under Federal Motor Carrier Safety Administration (FMCSA) authority must maintain minimum liability insurance levels based on the type of cargo they transport. These requirements are designed to ensure that trucking companies can financially respond to accidents and protect the public interest.

Minimum Insurance Requirements by Cargo Type

General Freight: $750,000 minimum combined single limit for vehicles weighing over 10,001 pounds. This covers most standard trucking operations transporting non-hazardous general commodities.

Hazardous Materials: $1 million minimum for trucks transporting hazardous materials that require placarding. The increased requirement reflects the higher risk associated with dangerous goods transportation.

High-Value Cargo: $5 million minimum for trucks transporting certain high-value commodities or passengers. This includes specialized haulers and companies transporting particularly valuable freight.

Household Goods: $750,000 minimum for moving companies and household goods carriers, with additional cargo liability requirements for customer belongings.

MCS-90 Endorsement Requirements

All interstate trucking companies must file an MCS-90 endorsement with the FMCSA, which ensures that insurance coverage meets federal requirements and provides a direct avenue for public claims against the insurance carrier. This endorsement is attached to your general liability policy and serves as proof of financial responsibility.

The MCS-90 endorsement guarantees that your insurance company will pay claims up to the minimum required limits, even if your policy has lapsed or been cancelled. This protection is crucial for maintaining your operating authority and avoiding costly compliance violations.

Coverage Options and Policy Structures

Combined Single Limit vs. Split Limit Policies

Combined Single Limit (CSL): Provides one overall limit that applies to all covered damages in a single accident. For example, a $1 million CSL policy can be used entirely for bodily injury, entirely for property damage, or any combination of both, providing maximum flexibility for claim settlement.

Split Limit Policies: Separate limits for different types of coverage, such as $300,000 per person for bodily injury, $500,000 per accident for total bodily injury, and $100,000 for property damage. While this structure may offer lower premiums, it can provide insufficient coverage for major accidents.

Aggregate Limits and Policy Periods

General liability policies typically include both per-occurrence limits and aggregate limits. The per-occurrence limit is the maximum amount the insurance company will pay for a single claim, while the aggregate limit is the total amount they will pay for all claims during the policy period.

For trucking companies, it's crucial to select adequate aggregate limits, especially if your operations involve higher-risk activities or frequent customer interactions. A single major accident or series of smaller claims can quickly exhaust your aggregate coverage, leaving your company exposed to additional liability.

Factors Affecting Premium Costs

Fleet Size and Vehicle Types

Insurance companies evaluate premium costs based on the number and types of vehicles in your fleet. Larger fleets generally receive better per-unit rates due to the law of large numbers, but also face higher overall premiums. The types of vehicles, their age, and their safety features all impact pricing.

Newer trucks with advanced safety technology, such as collision avoidance systems, electronic logging devices, and stability control, often qualify for premium discounts. Insurance carriers recognize that these technologies reduce accident frequency and severity.

Driver Records and Safety Performance

Driver safety records are among the most significant factors in determining trucking insurance premiums. Insurance companies thoroughly review Motor Vehicle Records (MVRs), conduct background checks, and evaluate driver experience levels when underwriting policies.

Companies with strong safety programs, regular driver training, and low accident rates can negotiate better premium rates. Conversely, fleets with poor safety records, frequent violations, or high driver turnover face substantially higher insurance costs.

Cargo Types and Operating Territory

The types of cargo you transport and your operating territory significantly impact liability exposure and premium costs. Hazardous materials, high-value goods, and fragile cargo all increase risk levels and insurance costs.

Operating territory also affects pricing, with urban areas generally commanding higher premiums due to increased traffic density, higher accident rates, and more expensive repair costs. Interstate operations face additional regulatory requirements and diverse state law considerations.

Claims Management and Best Practices

Immediate Response Protocols

Effective claims management begins with proper incident response procedures. All drivers should be trained on immediate post-accident protocols, including safety procedures, documentation requirements, and communication with emergency services and insurance representatives.

Key elements of proper incident response include: ensuring safety and calling emergency services if needed, documenting the scene with photos and witness statements, obtaining police reports when available, and notifying your insurance carrier immediately, ideally within 24 hours of the incident.

Documentation and Record Keeping

Thorough documentation is essential for successful claims resolution and can significantly impact settlement outcomes. This includes maintaining detailed driver logs, vehicle maintenance records, cargo manifests, and customer communications.

Modern fleet management systems can provide valuable data for claims defense, including GPS tracking, speed monitoring, and electronic logging device records. This information helps establish facts and can be crucial in disputed liability situations.

Selecting the Right Insurance Provider

Specialized Trucking Insurance Expertise

Choosing an insurance provider with specialized trucking expertise is crucial for obtaining appropriate coverage and competitive rates. Specialized insurers understand the unique risks facing trucking companies and can provide tailored solutions that general commercial insurers might miss.

Look for insurers that offer comprehensive trucking programs, including general liability, auto liability, cargo coverage, and physical damage protection. Bundling coverage with a single provider often results in better rates and simplified claims handling.

Financial Strength and Claims Service

Evaluate potential insurance providers based on their financial strength ratings from agencies like A.M. Best, Standard & Poor's, and Moody's. Strong financial ratings indicate the carrier's ability to pay claims promptly and maintain operations during economic challenges.

Claims service quality is equally important, as trucking companies need responsive support when accidents occur. Research customer reviews, ask for references, and inquire about average claim settlement timeframes and dispute resolution procedures.

Cost-Saving Strategies and Risk Management

Safety Program Implementation

Implementing comprehensive safety programs is one of the most effective ways to reduce insurance costs while improving overall operations. Successful safety programs include regular driver training, vehicle maintenance protocols, and performance monitoring systems.

Many insurance carriers offer premium discounts for companies that maintain strong safety scores, participate in industry safety programs, or achieve recognition from organizations like the National Safety Council or Truckload Carriers Association.

Deductible Management

Selecting appropriate deductible levels can significantly impact premium costs. Higher deductibles reduce premium payments but increase out-of-pocket expenses when claims occur. Trucking companies should evaluate their cash flow capabilities and risk tolerance when selecting deductible levels.

Some carriers offer "disappearing deductibles" that reduce over time with good safety performance, providing incentives for continued safe operations while managing upfront costs.

Future Trends and Technology Impact

Telematics and Usage-Based Insurance

Advanced telematics systems are revolutionizing trucking insurance by providing detailed data on driver behavior, vehicle performance, and route efficiency. Insurance carriers increasingly use this data to offer usage-based insurance programs that reward safe driving with lower premiums.

Telematics can monitor factors such as speeding, harsh braking, cornering forces, and hours of service compliance, providing real-time feedback to drivers and fleet managers while supporting insurance underwriting and claims investigation.

Autonomous Vehicle Considerations

As autonomous and semi-autonomous vehicle technology advances, liability insurance structures are evolving to address new risk scenarios. While fully autonomous commercial vehicles remain in development, advanced driver assistance systems are already affecting insurance pricing and coverage requirements.

Trucking companies should stay informed about technology developments and their insurance implications, working with knowledgeable agents to ensure coverage keeps pace with technological advancement.

Conclusion

Trucking general liability insurance is a critical component of successful commercial transportation operations, providing essential protection against the numerous risks inherent in the industry. From DOT compliance requirements to comprehensive coverage options, understanding the intricacies of general liability insurance enables trucking companies to make informed decisions that protect their assets and support their business objectives.

By working with specialized insurance providers, implementing strong safety programs, and staying current with industry developments, trucking companies can secure appropriate coverage at competitive rates while maintaining the financial protection necessary for long-term success. The investment in comprehensive general liability coverage is not just a regulatory requirement—it's a fundamental business strategy that supports sustainable growth and operational excellence in the competitive trucking industry.

Get Expert Trucking Insurance Guidance

Ready to secure comprehensive general liability coverage for your trucking operation? Our specialized insurance experts understand the unique challenges facing commercial transportation companies and can help you find the right coverage at competitive rates.

Get Your Quote Today